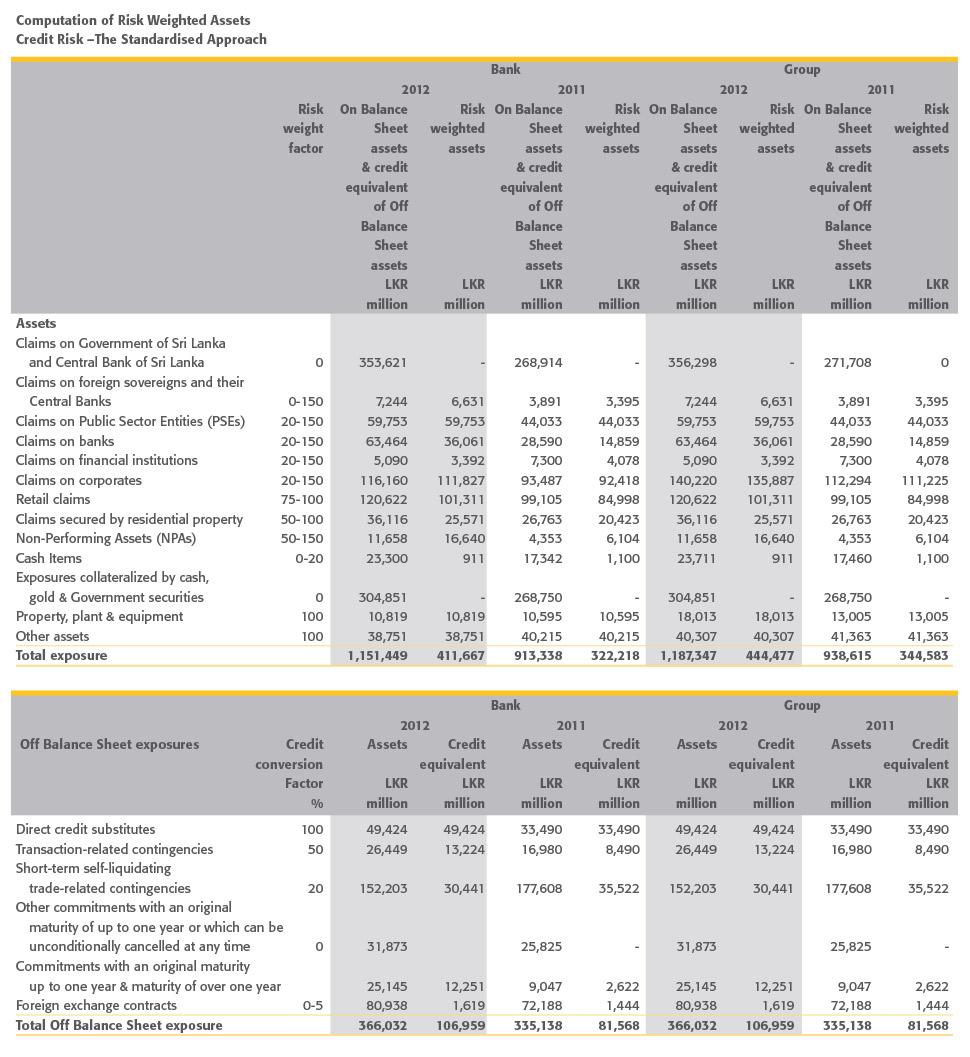

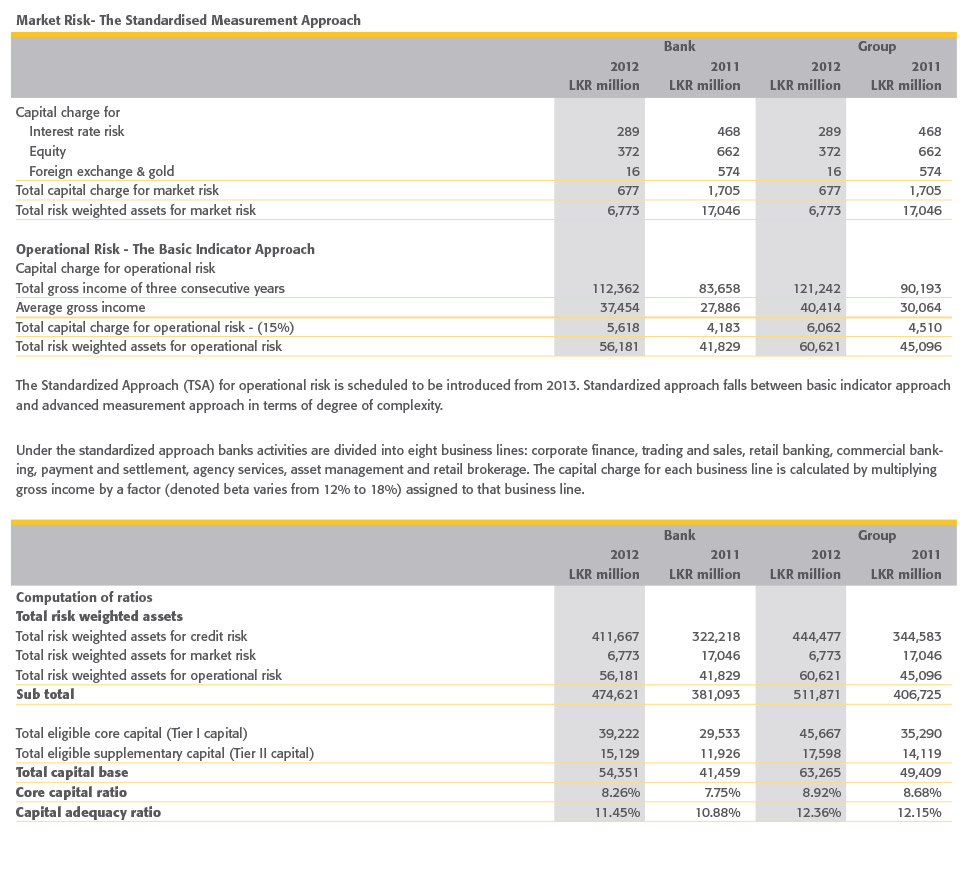

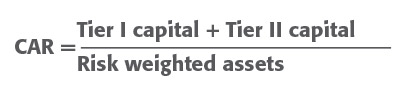

Capital Adequacy Ratio (CAR), also called Capital to Risk (Weighted) Assets Ratio (CRAR), is a measure of a bank's capital expressed as a percentage of risk weighted assets of credit, market and operational aspects of the banking business. It is a measure of financial strength of a bank which indicates it's ability to maintain adequate capital to meet any unexpected losses.

The objective of capital adequacy is to protect the banks themselves, their customers and the economy, by establishing rules to make sure that these institutions hold sufficient capital to ensure continuity of a safe and efficient market and able to withstand liquidity shocks and any foresee- able problems. Central Bank of Sri Lanka defines and monitors CAR to ensure that banks are not participating or holding investments that increase the risk of default and that they have enough capital to sustain operating losses while still honoring withdrawals, thereby maintaining confidence in the banking system.

Basel Committee on Banking Supervision housed at the Bank for International Settlements has established rules around capital require- ments commonly known as Basel Accords. Basel Accord is an agreement between bank supervisory authorities on the level of bank's capital with respect to bank's risk, as bank's capital is the "cushion" for potential losses.

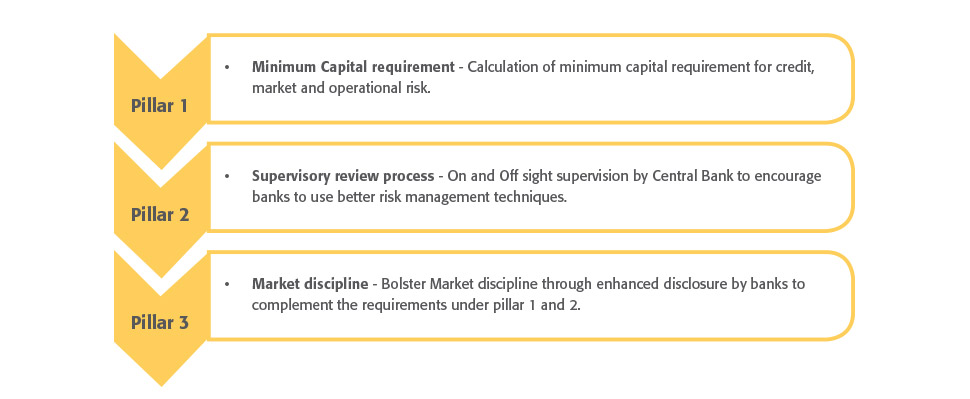

In 1988, the committee decided to introduce a capital measurement system referred to as Basel I. This framework has been replaced by a sig- nificantly more complex framework for the International Convergence of Capital Measurement and Capital Standards commonly known as Basel II, which structured three pillars, as depicted below.

The third Basel Accord is a comprehensive global regulatory stan- dard on bank capital adequacy, stress testing and market liquidity risk agreed upon by the members of the Basel Committee scheduled to be introduced from 2013. The third of the Basel Accords was developed in response to the deficiencies in financial regulation revealed by the global financial crisis. Basel III strengthens bank capital requirements and introduces new regulatory requirements to strengthen the regulation, supervision of the banking sector. The aim is to:

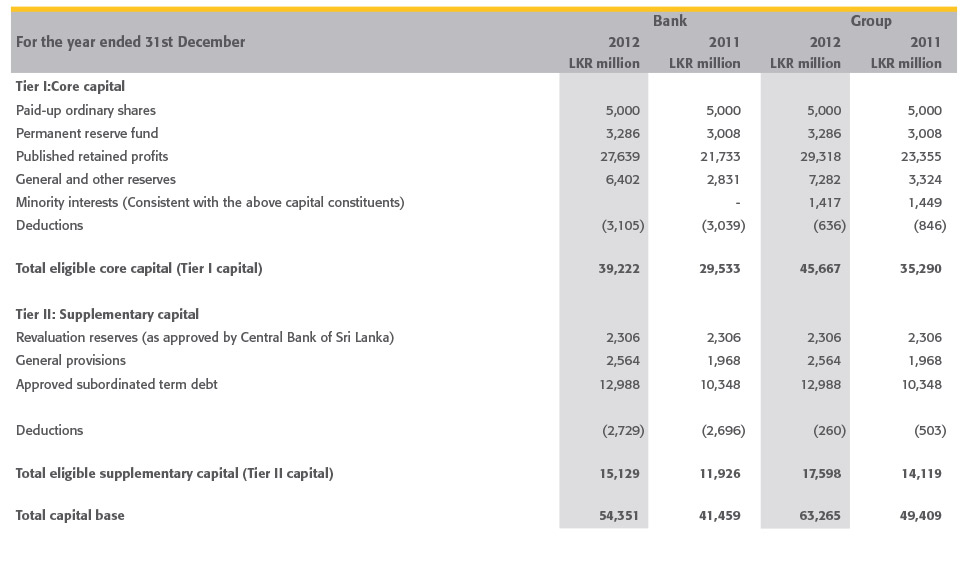

All commercial banks are required to compute capital adequacy on the solo basis and on the consolidated basis. Two types of capital are measured: Tier I capital , which can absorb losses without a bank being required to cease trading, and Tier II capital ,which can absorb losses in the event of a winding-up .Banks are required to maintain minimum of 5% of Tier I CAR and minimum of 10% of Tier I plus Tier II CAR as deter- mined by the Monetary Board.