Dear Stakeholders,

I am extremely proud to announce to you that your bank achieved the first ever trillion rupee balance sheet from among the Sri Lankan domestic banks. In 2009, we were brave enough to present our three year financial projection in keeping with the Government's Mahinda Chintana vision of achieving a per capita income of USD 4,000 by 2016. As a proactive move aimed at achieving this national goal, we took a forward looking stance to provide business opportunities to the masses, there by facilitating the financial and economic transformation as post war dividend. We even went to the extent of building a corporate plan slogan "One10Twelve" (rupees one trillion assets and rupees ten billion profit by year 2012) and put it on the public domain. I am deeply touched and extremely proud that our vision was right and we were able to achieve it in full, much ahead of the target date.

I am also happy to deliberate that this mammoth performance of your bank was achieved within very challenging global and domestic economic conditions. The year was full of challenges posed from several fronts. rising inflation, rupee depreciation, rising interest rates, drying up domestic liquidity and widening balance of payments presented a difficult environment for banks. The Bank therefore had to be very competitive in deposit mobilization by pressing the interest rate upwards. On the other hand, agriculture and allied value chains were affected by drought, heavy rains and floods in some parts of the island where our rural agricultural livelihood is concentrated. Our operational results and the targets were achieved despite all these difficulties.

In 2012 global economy did not emerge completely from the recession, which has continued since the economic crisis of 2008 - 2009. The Euro zone is still going through the aftermath shock of the financial crisis while the emerging economies too have not picked up from their slackened pace. So the world in 2012 experienced uncertain times posing a major concern to the local economic growth. With this global uncertainty, the overall Asian exports were affected.

Withstanding the unfavourable global environment, Sri Lanka continued its growth momentum. The timely supervisory measures taken by the regulators in the banking and financial sector along with fiscal and monetary measures maintained the discipline in the market, avoiding any possible adverse consequences.

We have certainly upheld the Government vision of public private partnership and continue in our efforts to support national development activities for economic progress. Our bank continued to assist the key sectors of the economy such as housing, agriculture and tourism. The aspirations of the Government that laid emphasis on economic development as well as improved quality of life guided our mission to serve a wide spectrum of the social strata.

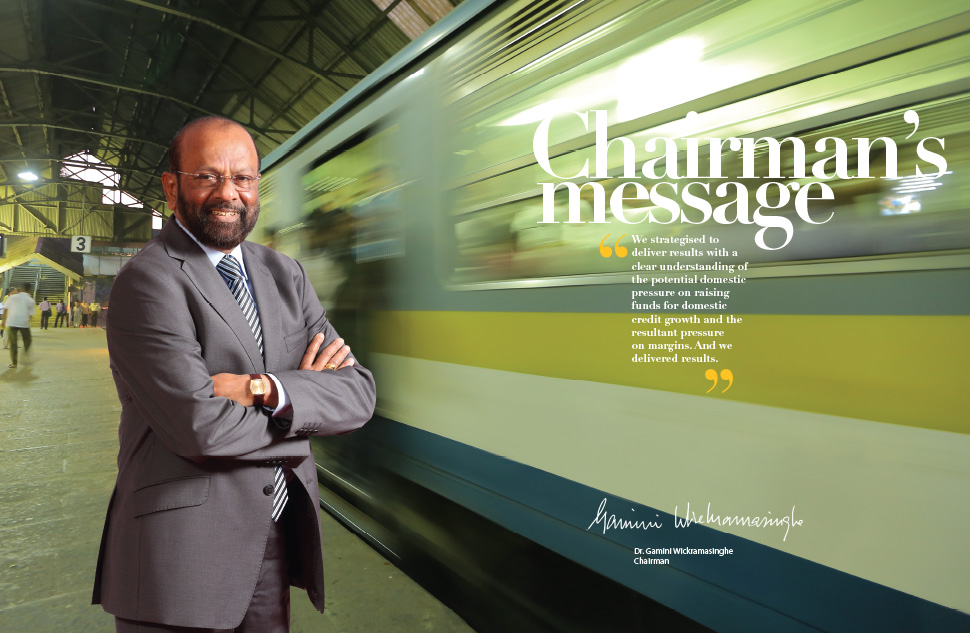

We strategised to deliver results with a clear understanding of the potential domestic pressure on raising funds for domestic credit growth and the resultant pressure on margins. And we delivered results. The assets of the group grew by 25% to LKR 1,079 billion whilst the loans and advances increased to LKR 733 billion, an increase of 27% over the previous year. The profit after tax is LKR 14.6 billion. The NPA Ratio of the Bank was checked to remain at 2.8% while deposits grew at 16%.

The capital adequacy is on a declining trend as a result of the increased asset growth over the last three years. Future expansion is also restricted, mainly due to the limitation in capital. Therefore, strengthening of the balance sheet with additional capital is the most significant priority in our prudent yet farsighted planning process.

Further, the Bank's recent listed rupee debenture issue was extremely successful and became the biggest ever debenture issue made by any financial institution in Sri Lanka, making it the fourth successful listed rupee debenture issue by the Bank.

During the period under review, we increasingly focused on expanding into a wider community oriented domestic financial inclusion mandate. We concentrated on the North and East in this effort to engage in economic development by expanding the branch network and increasing the man power in these provinces. Eleven branches were opened in the Northern Province on the same day. As a result the credit to North and East increased by LKR 7 billion in 2012.

We continued to expand in other provinces in order to consolidate and fortify our national footprint. Today, the network includes 600 customer service points after opening 34 new customer service points in 2012 whilst the growth of electronic banking services is demonstrated by the presence of 451 ATM points across the country. The number of service points reached 1,000 with the establishment of Puthukkudiyirippu service center.

During the year we also commenced a number of initiatives such as Leasing Pola to penetrate into the leasing market and we secured a decent share from the leasing market in the year 2012.

We expanded our correspondence relationships by adding 25 banks in 15 countries to our network. However, in view of the UN sanctions on Iranian transactions, the Bank had to abandon all Iranian correspondence relationships during the year.

The Bank facilitated foreign remittances amounting to LKR 283 billion to the country during the year 2012, an increase of 15% over the previous year and continued to lead the inward remittances with 38% market share. This has been done by strengthening our relationship with the operating agents throughout the world, in addition to the improvements made to our owned proprietary web based fund transfer system. Several promotional activities were launched both locally and internationally to enhance the customer base.

Our major achievement in international operations is the issuance of a USD 500 million bond, which was drawn up mainly from Asia, Europe and America. This was the first ever listed bond from a non-sovereign entity from Sri Lanka which set the floor open for others to follow suit. The bond was over-subscribed by 7.7 times which is a testimony to acknowledge our credentials on our international acceptance. As part of this process we obtained international ratings from Fitch and Moody's which rated us on par with Sri Lanka's sovereign rating.

Our sustainability speaks of our organisational culture and values. Our CSR initiatives were aimed at improved community and social bases through agro-based livelihood, literary and cultural development and working alongside the tri-lingual initiative launched by President Mahinda Rajapaksa aimed at making sure that all Sri Lankans learn the three main languages; Sinhala, Tamil and English towards better ethnic harmony.

In upholding its objectives of meeting the needs of the people and contributing to the sustainable development of the country, the Bank initiated several CSR activities. Financial assistance provided for the Deegavapi Restoration Project, where the Bank funded the accommodation costs of labour, excavations and identified infrastructure facilities proved to be one of the major CSR activities during the year. Further aiming for sustainable economic development, the Bank undertook to re-build the Jaffna railway station which would facilitate the communities in the North and South to interact within socio economic groupings.

Competitively, the information economy places high demands on our business. Continuous innovation is required to meet rapidly developing consumer preferences, a trend not limited to banking, while at the same time it is essential to provide robust and resilient operational capabilities. Clearly our business survives because of the quality of our people, systems and processes. Our people's technical ability, their market knowledge and experience in the industry make Bank of Ceylon's story more attractive. But we were aware of the challenges in a highly changing and a demanding consumer landscape that require investment in human capital, technology and infrastructure. And we will continue to invest along these lines.

We approach 2013 watching a number of potential challenges on our radar. As Europe and America are undergoing a period of reforms, the impact of such reforms will be felt by every part of the world. The banking sector will continue to face the liquidity and asset quality challenges given the current interest rate regime. More international funding will be focused to ease the domestic fund mobilisation competitions with a view to stabilise the interest rates. Expanding the man power base, investment in building human capital, upgrade on present technology platforms and introducing new technology based delivery solutions are lined up for 2013 to position the Bank to face future challenges.

On behalf of the Bank, I would like to place on record our gratitude to customers for their sustained support and patronage. The contribution made by Auditors, Legal Advisors, Consultants and Correspondents is greatfully acknowledged. The stance taken by the trade unions of the Bank towards the progress of the Bank is deeply appreciated.

I am grateful to the General Manager, Senior Management and staff for the relentless support rendered to me and the Bank over the years.

My sincere gratitude goes to His Excellency the President, Honourable Deputy Minister of Finance and Planning, the Secretary to the Treasury and the Governor of the Central Bank of Sri Lanka. My Board of Directors has always been supportive and I wish to thank them all and wish them well.

In conclusion, I wish to state that this is my final report as the Chairman of Bank of Ceylon. I will stand down as Chairman on 8th January 2013 and hand over to my successor the task of taking forward the Bank to new heights.

I wish you all and the Bank of Ceylon very best.

Dr. Gamini Wickramasinghe

Chairman

7th January 2013

Colombo